How to Create a Simple Monthly Budget That Actually Works

Managing your money can feel overwhelming, especially if you don’t know where to start. But creating a monthly budget doesn’t have to be complicated. A simple, clear plan can help you see where your money goes, reduce stress, and even save for your goals. In this guide, we’ll break down the steps to create a monthly budget that works for you.

Step 1: Track Your Income

Before you can plan your spending, you need to know how much money you have. Start by listing all your sources of income. This could include your salary, freelance work, side hustles, or any other regular income.

If your income varies month to month, consider using an average from the past three months. For example, if you earned $2,500, $3,000, and $2,800 over the last three months, your average monthly income would be $2,767.

Knowing your total income is the foundation of a budget. It sets the limit for how much you can spend each month.

Step 2: List Your Expenses

Next, write down all your monthly expenses. Start with fixed expenses—these are bills that stay the same each month. Examples include:

- Rent or mortgage

- Utilities like electricity and water

- Loan payments

- Internet and phone bills

Then, list variable expenses. These can change month to month, like:

- Groceries

- Gas or transportation costs

- Dining out

- Entertainment

- Personal care items

It’s easy to forget some small expenses, like subscriptions or coffee shop visits. Review bank statements or receipts from the past month to catch everything.

Step 3: Categorize and Prioritize

Once you have a complete list of expenses, group them into categories. A simple way is to use three main categories:

- Needs – Essentials you can’t skip, like rent, utilities, groceries, and transportation.

- Wants – Non-essentials, like dining out, hobbies, and entertainment.

- Savings and Debt Repayment – Money set aside for future goals or paying off debt.

Prioritizing helps you see where you might be overspending. If your wants category is taking a large chunk of your income, it may be time to cut back and redirect funds toward savings or debt.

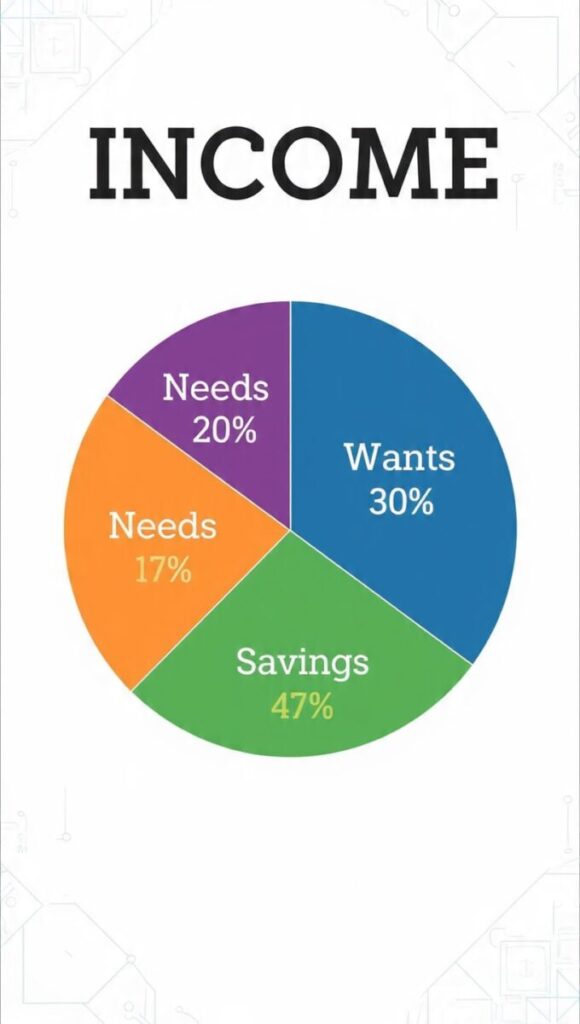

Step 4: Set Spending Limits

Now it’s time to assign a spending limit for each category. A popular method is the 50/30/20 rule:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

For example, if your monthly income is $2,500:

- $1,250 for needs

- $750 for wants

- $500 for savings and debt repayment

These numbers aren’t strict. Adjust them based on your priorities. If you’re trying to pay off debt quickly, you may allocate more to savings and less to wants.

Step 5: Track Your Spending

Creating a budget is only useful if you stick to it. Track your spending throughout the month to make sure you don’t go over your limits.

You can track your expenses in different ways:

- Spreadsheet – Use Excel or Google Sheets to list income, expenses, and remaining balance.

- Budgeting app – Apps like Mint, YNAB, or PocketGuard make tracking easy and automatic.

- Pen and paper – A simple notebook works if you prefer a hands-on approach.

Check your spending weekly. If you notice you’re overspending in one category, adjust your habits or shift money from another category.

Step 6: Plan for Irregular Expenses

Some expenses don’t occur every month, like car maintenance, annual subscriptions, or medical bills. To avoid surprises, include a small monthly “buffer” in your budget for these irregular costs.

For example, if you know your car insurance costs $600 annually, set aside $50 per month. By the time the bill is due, you’ll already have the money saved.

Step 7: Build Savings Goals

A budget isn’t just about controlling spending—it’s about planning for your future. Decide what you’re saving for, whether it’s an emergency fund, a vacation, a home, or retirement.

- Emergency fund – Ideally, you want 3–6 months of living expenses saved.

- Short-term goals – These might include a new phone, a trip, or a wedding.

- Long-term goals – Retirement accounts, investing, or buying property.

Allocate a portion of your income to these goals each month. Even small amounts add up over time.

Step 8: Review and Adjust

Your budget should be flexible. Life changes, and so do your income and expenses. At the end of each month, review your budget:

- Did you stick to your limits?

- Did unexpected expenses arise?

- Can you increase your savings or reduce your spending next month?

Adjust your budget based on your findings. This helps you stay realistic and avoid frustration.

Step 9: Keep It Simple

The most effective budget is one you can maintain. Don’t overcomplicate it with dozens of categories or rules. A simple budget that tracks income, spending, and savings is more useful than an overly detailed one you’ll give up on.

Step 10: Make It a Habit

Finally, the key to budgeting success is consistency. Make reviewing your budget a monthly habit. Set reminders to check your spending mid-month and at the end of the month. Over time, budgeting becomes second nature, and you’ll gain better control over your finances.

Creating a simple monthly budget doesn’t need to be intimidating. By knowing your income, listing your expenses, setting limits, and tracking your spending, you can take control of your finances. Remember, the goal isn’t perfection—it’s progress. Small, steady changes will help you save more, reduce stress, and reach your financial goals faster. Start this month, and you’ll be surprised at how much difference a simple budget can make.